The $200B Foodservice Market Is Going Digital

The Moment Is Here

The $200 billion independent foodservice distribution market has been described as “about to go digital” for at least a decade. That framing is no longer accurate.

It’s going digital now. Not as a forecast. As a measurable shift.

At last count, the network we work across spans 220+ distributors, 140,000+ operators, 16,000+ manufacturers, and over $22 billion in GMV tracked through the platform. Those aren’t projected numbers from a slide deck. Those are live transaction counts

from the last twelve months.

Five years ago, these numbers were a fraction of what they are today. Five years from now, they’re going to be multiples. The independent distribution segment — long considered the most analog, relationship-driven part of food supply — is digitizing faster than almost any industry observer predicted.

The reason it’s happening now, and not earlier, is worth understanding. So is what it means for manufacturers, for independent distributors, and for the operators those distributors serve.

Why Now?

Three forces converged, and none of them were software.

The first is consolidation pressure. The Sysco-Jetro acquisition in late 2025 was the clearest signal to the industry that national distributors are actively acquiring into independent territory. Sysco didn’t pay billions for Jetro because they wanted more broadline volume. They paid for deeper presence in independent restaurant channels — the customer base that independent distributors have historically owned.

Independents understood the implication immediately. A national competitor with Sysco-scale economics, now positioned to compete on the same customer sets, changes the math on every local account. The independent distributor’s traditional moat — relationship depth, service flexibility, local knowledge — is still real, but it has to be paired with technology that matches scale economics. Software stops being a nice-to-have and becomes a defensive imperative.

The second is generational transition at the operator level. Restaurant owners who started their businesses in the 1990s are handing them off to operators who grew up with smartphones, marketplaces, and instant fulfillment. The new generation expects their foodservice ordering to feel like the consumer commerce they use every day. The distributors who can deliver that experience are picking up share from the ones still running on phone calls and paper order guides.

The third is manufacturer investment. Manufacturers facing flat retail foodservice growth have been looking for scalable ways to drive incremental sales through independent channels. The traditional route — more DSR coverage, more rebate programs, more trade spend with poor attribution — doesn’t scale. Digital campaigns running through distributor platforms do. Manufacturers are actively pushing budget toward channels where ROI is measurable, and that pressure is accelerating distributor digital investment.

Put those three forces together, and the sector that took two decades to meaningfully digitize its ordering is now compressing a decade of change into two or three years.

“The independent foodservice market isn’t digitizing because software got better. It’s digitizing because the economic pressure on the status quo hit a breaking point.”

What the Numbers Actually Show

When you aggregate data across 220+ distributors running on a common platform, patterns emerge that no single distributor could see.

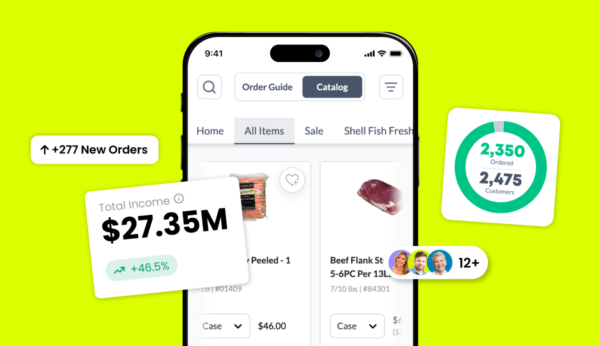

Operator digital adoption among distributors live on the network averages 65-75% of active accounts within twelve months of deployment. The leaders are above 85%. That’s total operator count, not pilot accounts.

Digital order frequency among adopted operators is 2.3x higher than phone-order frequency was for the same accounts before digital. Operators who can order at 10pm or 6am order more often, and they place smaller, more frequent orders, which is better for distributor working capital.

Average order value on digital orders is 14% higher than the pre-digital baseline for the same operator. The reason is simple — operators browsing a digital catalog with good imagery and recommendations see more products they want to order than they did when they were dictating an order to a DSR from memory.

Manufacturer-funded campaigns, targeted at specific operator segments through the digital ordering experience, are returning an average of $14 in attributable sales for every $1 invested. That ratio has held across hundreds of campaigns with different products, geographies, and operator types. It’s not a one-off result. It’s the baseline of what attribution-native campaigns look like.

At the network level, these numbers translate to structural changes in how the foodservice supply chain operates. Manufacturers are able to run real campaigns at the operator level, with real measurement. Distributors are able to capture order flow that used to happen outside their systems — nights, weekends, emergency orders — because the digital channel is always open. Operators are seeing products they didn’t know their distributor carried.

The Independent Advantage, Digitized

The traditional advantages of independent foodservice distributors — relationship, flexibility, local knowledge, service — aren’t going away. They’re the whole reason independents still own 60%+ of the restaurant-level market despite decades of consolidation pressure.

What’s changing is that these advantages now need to be paired with digital infrastructure to remain competitive. The independent distributor with a great sales force and a mediocre e-commerce platform is going to lose share to the independent distributor with a great sales force and a strong digital platform — even if the second one has fewer DSRs.

The reason is compound. Digital ordering doesn’t replace the DSR relationship. It amplifies it. A DSR whose operator places routine orders digitally has more time for strategic conversations with that operator. The relationship deepens instead of flattening. The operator still values the DSR relationship, but now the DSR is freed from taking down the standard weekly order and can focus on new product introductions, category expansion, and account growth.

“Independent distributors don’t win by becoming national distributors. They win by digitizing the service model that independents always offered better.”

This is the part that’s lost when people debate whether independents can “survive” consolidation. The framing is wrong. Independents aren’t going to survive by being smaller versions of Sysco. They’re going to survive by being better versions of what independents have always been — and doing it at a scale that only networked technology makes possible.

The Independent Advantage, Digitized

For manufacturers, the digitization of independents solves a long-standing measurement problem.

In retail, manufacturers have had SKU-level scan data for decades. They can see what’s selling, where, to whom, and at what price. That visibility drives trade spend efficiency, category management, and new product launches.

In foodservice, scan data never existed. Manufacturers were flying blind. They knew total sell-in to distributors, but they couldn’t see sell-through to operators. They funded promotions they couldn’t measure, invested in DSR coverage they couldn’t audit, and relied on survey data that was usually six months stale.

A networked foodservice platform changes that. A manufacturer running campaigns across 220+ distributors now has operator-level visibility into what’s selling, to which operator types, in which geographies, at what rate, and in response to which kinds of promotion. That visibility makes every subsequent investment smarter. The manufacturers who figure out how to use this data have a material competitive advantage over the ones who don’t.

McCormick is the clearest public example. McCormick is driving $100M in annual foodservice sales through independent distributors on the network — a large portion of it through digital Influence campaigns that didn’t exist three years ago. That’s not a one-off. It’s a new category of manufacturer GTM that’s available to any brand willing to invest in attribution-native marketing.

The Sysco Perspective

For those of us who have spent our careers inside Sysco, the digitization of independent foodservice distribution has a specific resonance.

The national distributors built their scale advantage partly on technology — proprietary systems, data infrastructure, and category management tools that independents couldn’t afford to replicate. For thirty years, independent distributors have had to compete on relationships despite being at a structural tech disadvantage.

What’s changing now is that a networked platform gives independents access to infrastructure that previously required national-scale investment to build. Catalog data from 16,000+ manufacturers. Operator intelligence from 140,000+ restaurants.

Manufacturer campaign execution with transaction-level attribution. AR and embedded payments infrastructure. Fleet and route optimization tools. Each of these used to require a Sysco-scale IT budget to build internally. Now they’re infrastructure services that a 500-operator independent can plug into.

That levels the playing field in a way the industry hasn’t seen in a long time. The independents that adopt early are going to open a gap on the ones that don’t. And the independents that adopt fast are going to capture share from both the laggards and the national competitors who are trying to move down-market.

What Comes Next

Three predictions, based on the current trajectory.

First, the pace of digital adoption among independents is going to accelerate over the next 24 months, not decelerate. The Sysco-Jetro consolidation pressure is not going to reverse. Operator generational change is not going to pause. Manufacturer demand for attributable channels is going to intensify. Every one of those forces is still building.

Second, distributors that are still running fragmented technology stacks — separate systems for ordering, payments, fleet, CRM, analytics — are going to face a choice in the next two years: consolidate onto a unified platform or accept a structural cost disadvantage. The integrated-platform distributors are going to be more efficient, more responsive, and more attractive to manufacturer investment. The fragmented-stack distributors are going to be squeezed.

Third, the manufacturer investment story is going to become impossible to ignore. The McCormick $100M number is going to be one of many public examples within 18 months. Once five or six major brands are publicly citing their foodservice digital investment ROI, trade spend allocation across the industry will shift meaningfully toward attribution-capable channels. That shift will fund the next wave of digital distributor adoption.

The $200B independent foodservice market isn’t about to go digital. It is going digital. Measurably, right now. The distributors, manufacturers, and operators who position for that shift in the next 24 months are going to define the competitive landscape for the decade that follows.

If you want to see what the digital shift looks like at the network level — what 220+ distributors and 140K operators are actually doing differently — we’d like to walk through the data with you