How a Regional Produce Distributor Grew AOV 22% in 90 Days — Without Adding a Single Sales Rep

TLDR

- A regional produce distributor grew AOV 22% in 90 days without adding sales reps, routes, or new headcount.

- The lift came from four connected levers: catalog enrichment, fleet-aware DSR intelligence, manufacturer-funded campaigns, and embedded payments.

- Better catalog data helped operators complete more of their order digitally instead of splitting orders between app and phone.

- DSR intelligence turned routine account visits into strategic conversations that recovered volume and deepened operator relationships.

- The case shows how independent distributors can grow by becoming more integrated, not simply bigger.

The Starting Point

A mid-sized produce distributor in the Mid-Atlantic region came to us looking for growth. Their operation looked like most independents: roughly $85M in annual revenue, 14 trucks, 320 active operators concentrated across restaurants and institutional accounts, a sales team of 9 DSRs, and an order book that was still 70% phone and text-message driven.

They’d tried digital ordering once before with a generic B2B platform. Adoption peaked around 22% and stalled. Operators didn’t see a reason to change what was working on the phone. DSRs didn’t push the platform because it didn’t make their jobs easier. Leadership was close to writing off digital as “not a fit for produce.”

Their specific objection was one we hear constantly from produce distributors: daily pricing, short product windows, perishability, and delivery-route dependency make produce “different” from broadline. A generic e-commerce platform can’t handle the operational reality. They weren’t wrong. They just needed a platform that was designed for produce-grade constraints, not retrofitted for them.

Twelve weeks after deploying on our network, they reported the following:

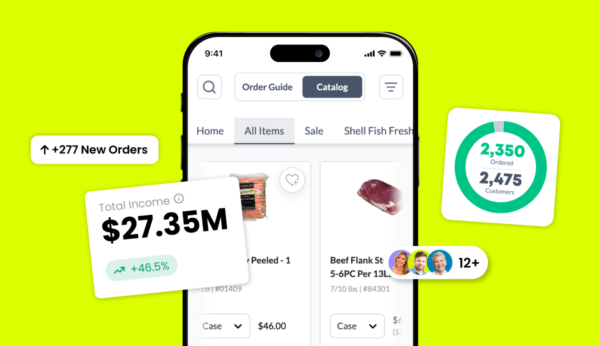

- Average order value up 22%

- Order frequency up 31%

- DSO reduced by 4 days

- Operator digital adoption at 74%

- DSR-reported time savings of 6-8 hours per rep per week

Total incremental revenue attributable to the digital shift in the first 90 days was in the $1.8-2.1M range. No new headcount. No change in route structure. No acquisition activity.

Here’s what actually moved the numbers.

The distributor didn’t grow by adding more people. They grew by making the same team, routes, catalog, and operators work harder together.

Lever One — Catalog Depth, Not Catalog Breadth

Most distributors think of catalog work as “get more SKUs into the system.” That’s mostly wrong, especially in produce.

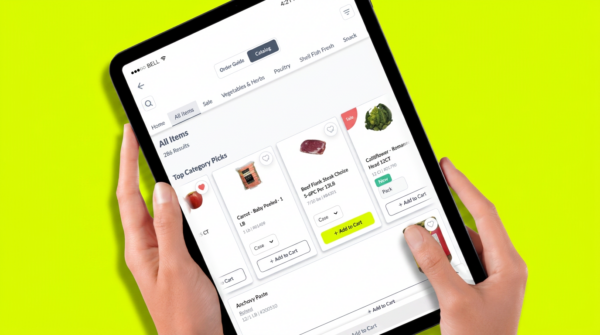

The first 30 days of the engagement, we worked with the distributor’s merchandising team to enrich their existing SKU set rather than expand it. Real imagery from their actual product, not stock photos. Pack size and grade attributes consistently applied across every item. Origin and seasonal availability data populated. Flavor profiles and culinary use cases tagged for restaurant-relevant search.

The net effect was a catalog that looked substantially different at the operator level without any new SKUs added. Operators browsing on mobile in the morning could find products faster, filter by what they actually needed (organic, origin, case size), and see high-confidence visuals instead of generic thumbnails.

Order completeness improved measurably. Operators who had been ordering 8-12 items per order started ordering 14-18 items per order — not because they were buying more product overall, but because they were completing their order on the platform instead of calling the DSR to add the last four items.

Average order value didn’t jump because operators were spending more. It jumped because operators were finishing the order in the platform instead of splitting it between digital and phone.

Lever Two — Fleet-Aware DSR Intelligence

The produce distributor’s DSRs were spending a significant portion of their day taking down orders they could have been having strategic conversations about. The generic platform they had used before didn’t change that dynamic — it just moved some of the orders from phone to app without changing what DSRs did.

On our network, DSRs got real route context tied to their daily activity. Before each visit, they saw:

- The operator’s 30-day ordering trend

- Which products had shifted in the last 7 days

- New SKUs the operator hadn’t yet tried that similar operators in the territory had adopted

- Delivery history, including any quality disputes or short-shipments

- Account health indicators: order frequency decline, basket shrinkage, competitor product presence

DSRs used this intelligence to turn routine visits into strategic conversations. An operator whose broccoli crown orders had dropped 18% got a conversation about why — and in three separate cases in the first 60 days, the DSR uncovered that the operator was buying from a competitor who had started running weekly specials. The DSR responded with a counter offer, and the volume came back.

A routine visit with an order take turns into a five-minute conversation. A fleet-aware visit turns into a fifteen-minute strategic conversation that uncovers $800-$2,000 per month in recoverable volume.

That dynamic is the difference between DSR time being a cost center and DSR time being the distributor’s competitive advantage.

Catalog work lifted order completeness. DSR intelligence lifted account-level depth. Together, they compounded into 22% AOV growth.

Lever Three — A Single Manufacturer-Funded Campaign

Sixty days in, we ran a single manufacturer-funded cashback campaign with one of the produce distributor’s strategic brand partners. The target: premium salad greens, specifically targeted at fine-dining and hotel accounts in the distributor’s territory.

Budget: $18K funded by the manufacturer. Campaign window: 30 days. Targeting: 80 operators in the premium segment, based on segment tags and historical salad purchase velocity.

Results at day 30:

- Salad green volume up 34% among targeted accounts

- 17 of the 80 targeted operators adopted the brand who hadn’t been carrying it before

- Total attributable incremental sales: $224K

- ROI: 12.4x on the manufacturer’s campaign

The distributor captured that volume at normal margin. The manufacturer got measurable sales lift plus operator-level adoption data they’d never had before. The operators got cashback they actually saw credited in their account. No party to the transaction had a bad outcome.

This is the manufacturer Influence mechanic in action — and it’s an entirely new lever for produce distributors who’ve historically been locked out of this kind of marketing money because their pre-digital systems couldn’t execute or measure it.

Lever Four — Payments Inside the Flow

The fourth lever was less visible but arguably the biggest working-capital unlock.

Before the engagement, this distributor’s AR process looked like most independents’: invoices emailed after delivery, a statement cycle on the 15th of each month, and a two-person AR team chasing late accounts. DSO sat at 43 days.

After moving to a platform where payment happens inside the ordering flow, where operators can see open invoices the same time they’re placing new orders, and where proof of delivery automatically triggers the invoice — DSO dropped to 39 days within 90 days.

Four days of DSO on $85M annual revenue is about $930K in working capital returned to the business. Real money. Not a soft metric. Cash that could fund inventory expansion, truck capacity, or margin compression on a strategic account.

The AR team didn’t get smaller. They just stopped chasing and started managing exceptions. Most accounts now paid on time because paying was the most frictionless action on the platform. AR intervention focused on the accounts where intervention actually changed the outcome.

What Didn’t Happen

A few things worth calling out that didn’t drive these numbers:

No new DSRs were added. The sales team stayed the same size. No new routes were added. Delivery capacity stayed constant. No acquisitions. No opportunistic new customer wins. No M&A activity. No major price change. The distributor didn’t compete on price. No marketing push to end operators. All operator adoption was driven by DSRs and the platform experience.

Everything in the 22% AOV lift came from internal leverage: the same operators, served by the same DSRs, out of the same warehouse, with a better platform underneath them.

What It Cost

Platform subscription and implementation: a low-six-figure annual investment.

Time from the leadership team: the CEO and VP Sales put roughly four hours per week into the deployment for the first 60 days — not to run it, but to sponsor it. The ops team put in a concentrated 30-day effort on catalog enrichment, then returned to normal workload.

Operator-facing disruption: essentially none. Operators who preferred to phone in orders still could. DSRs who preferred to call on accounts still did. The change was additive. The digital channel expanded the ways operators could order without taking anything away.

The Math

In return for a low-six-figure annual investment, the distributor generated $1.8-2.1M in incremental 90-day revenue and ~$930K in returned working capital from DSO reduction. The payback period on the platform investment was under 45 days.

Not every distributor will hit these exact numbers. Some will do better, especially in verticals like meat and seafood where AOV has more headroom. Some will take longer — especially distributors whose catalog needs more extensive work or whose DSR team needs more ramp time to use the intelligence layer.

But the direction is consistent across the network. Distributors who move from fragmented, generic e-commerce platforms to a networked foodservice-native platform tend to see:

- AOV gains of 12-25% in the first year

- Order frequency gains of 15-35%

- DSO reduction of 4-10 days

- DSR time savings that translate to new account acquisition capacity

Those numbers compound. The distributor in this case study is now three quarters further down the curve, and the trajectory has held.

What Independents Can Actually Do

The takeaway from this case study isn’t that one produce distributor got lucky. It’s that the underlying mechanics — catalog depth, fleet-aware DSR intelligence, manufacturer-funded campaigns, embedded payments — are available to every distributor on the network, and they compound when used together.

The reason they compound is that they’re all running on the same platform. Catalog investments improve the search experience which drives order completeness which surfaces products the DSR can promote which creates the data footprint manufacturers fund campaigns against. Each lever makes the next one stronger.

On a fragmented stack — separate ordering, separate payments, separate CRM, separate analytics — these layers don’t reinforce each other. They sit next to each other and get used partially.

Independent distributors don’t need to be bigger to win. They need to be more integrated. That’s the lesson the $200B independent market is going to learn in the next three years, and the distributors who learn it first are going to be disproportionately rewarded.

If your digital platform has plateaued and you’re looking for the next 20% of growth without adding headcount, we’d like to show you what this looks like on your specific book of business.